When you delve into the intricate world of insurance policies, you may find yourself confronted with a plethora of terms that can quickly become perplexing. One such term that frequently arises is “Name of Insured.” Have you ever paused to ponder what this phrase truly signifies? Why does it wield so much importance in the realm of insurance? Understanding the nuances of this concept is not merely an academic exercise; it can have significant implications for policy coverage and legal liabilities. Buckle up as we navigate through the thoughtful and sometimes convoluted landscape of insurance terminology.

Defining the Term

The “Name of Insured” refers to the individual or entity that is covered under an insurance policy. In essence, this person or organization stands to benefit from the protections afforded by the policy in question. But why is clarity around this terminology vital? Imagine a scenario where you believed you were comprehensively covered for a particular event only to discover, upon filing a claim, that the insurance protection was limited or did not apply at all. Misunderstanding who is named in the policy can lead to this very dilemma, underscoring the necessity of apprehending the term fully.

Types of Insured Parties

Within the umbrella of insurance policies, the “Name of Insured” can be categorized in various ways. The most common types include:

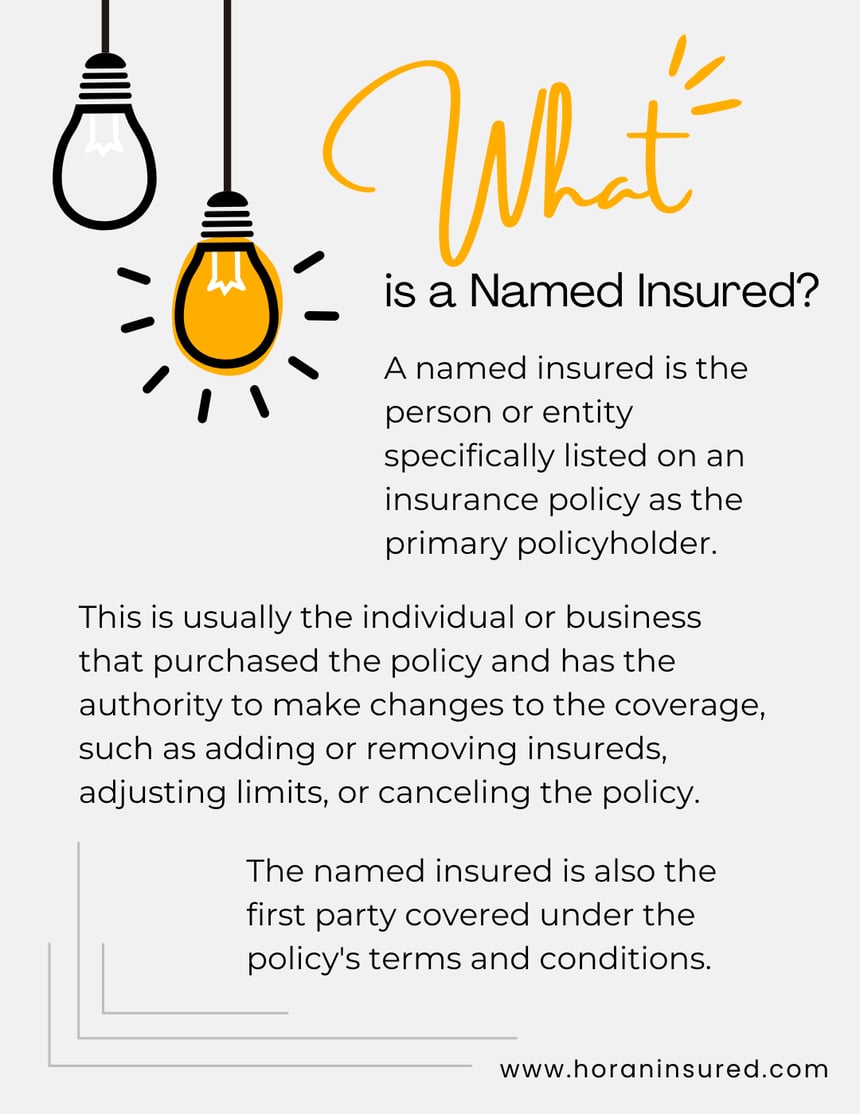

- Named Insured: This denotes the primary individual or entity specifically listed on the insurance document. They bear the brunt of the contract’s obligations and rights.

- Additional Insured: This refers to additional entities or individuals who are afforded some level of coverage under the policy. They are not the primary insured but still benefit from the protections therein, often used in business environments where multiple parties might share risk.

- Pending Insured: This is a temporary designation for an individual or entity awaiting final approval of their insurance coverage.

Each category serves a distinct purpose and is critical in different contexts, making it imperative to ascertain who exactly is covered under a given policy.

The Role of the Named Insured

The role of the named insured is pivotal. They not only enjoy the security provided by the insurance policy but also have specific responsibilities, including the prompt payment of premiums and adherence to the terms specified. Think of them as the keystone in an arch; while they reap the rewards of coverage, they also uphold the structure of the agreement. If the named insured fails to comply with any policy conditions, the entire agreement can be jeopardized, leaving all parties uncovered.

Implications for Additional Insureds

Consider the additional insureds for a moment; they may appear to have it easy since they enjoy access to coverage without bearing the financial responsibilities typically associated with a policy. However, there’s a nuance here that belies the initial impression. Coverage for additional insureds is often limited, contingent on the scope agreed upon in the contract. For instance, if a subcontractor is listed as an additional insured on a contractor’s policy, they might only be covered for claims arising directly from the contractor’s operations—leaving a gaping hole in protection for activities outside the defined parameters.

Challenging Scenarios in Insurance

Imagine facing a legal challenge in which understanding the “Name of Insured” becomes paramount. A car accident occurs involving a vehicle owned by a business that is leased to an individual who is not listed as a named insured. When a claim is filed, the insurance company raises the question of coverage. Will the individual driver face financial ruin, or will a comprehensive understanding of their rights enable a favorable resolution? This is the kind of scenario that illustrates the tangible impact of understanding insurance terminology.

How to Navigate Insurance Policies

In navigating the sometimes murky waters of insurance policies, transparency is your best ally. Here are actionable steps to employ:

- Read Your Policy: This might sound rudimentary, but a meticulous review of your insurance documentation can unveil the myriad intricacies linked to the “Name of Insured.”

- Ask Questions: Don’t hesitate to reach out to your insurance agent or broker with any queries you may have. They are your first line of inquiry and can elucidate terms.

- Update Regularly: As life circumstances evolve—be it through marriage, business expansion, or additional assets—review and update your policy to ensure all relevant parties are properly insured.

Conclusion

Understanding what “Name of Insured” denotes is an essential underpinning of navigating the complexities of insurance policies. Whether you are the primary insured or acting in the capacity of an additional insured, knowing your role can mitigate risks and protect against potential financial calamities. Insurance, at its core, is about managing uncertainty, and an informed approach can provide the fortress of security against the unpredictable nature of life and business. So, the next time you peruse your insurance policy, remember: clarity can shield you from unexpected challenges that lie ahead.